Many years ago while reading the Berkshire Hathaway (BRK.A) 1986 Letter to Shareholders, I discovered Warren Buffett?s ratio, which he calls "Owner Earnings". And to my amazement, in a little footnote Mr. Buffett actually explains how to use it and basically states that it is one of the key ratios that he and Charlie Munger use in analyzing stocks.

Due to the popularity of my ?Buffett?s Favorite Ratio? articles, I have gotten many emails asking me to analyze Apple in that context. The following is my analysis of Apple (AAPL) and its industry using Mr. Buffett's ratio. For those new to this type of analysis please look here.

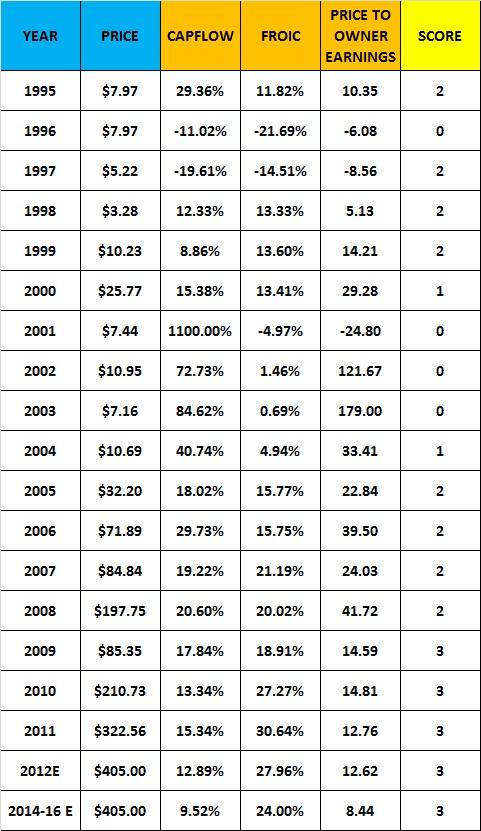

I would like to start this analysis by first showing everyone how Apple has done from a historical owner earnings perspective, going back to 1995: (Click to enlarge)

As you can see from the data above, buying Apple when its price to owner earnings broke below 15 in 2009 would have been the best time to buy its stock. Buying a company's stock when it breaks below that specific number on a price to owner earnings basis is key in doing this type of analysis. I proved that point in my back test of the DJIA 30 Index for the 60 year period of 1950-2009.

From a CapFlow perspective, Apple has consistently stayed below 50% since 2004 and the chart below will show you what that has meant for the company?s stock price: (Click to enlarge)

CapFlow is a key indicator of how management is conducting its cost controls. Had you been using this system at the time, you would have seen Apple's CapFlow drop from 84.62% in 2003 to 40.74% in 2004. Management cut costs by 51.85% in that year and proceeded to drop CapFlow in 2005 to 18.02%. This miraculously amounted to another drop of 55.78%. Management was clearly in charge of their destiny at the time because in just two years they were able to drop Apple's CapFlow by some 78.07%. This was a key breaking point for the company and because management has continued to keep the company's CapFlow low, it has been able to generate some serious Owner Earnings growth rates.

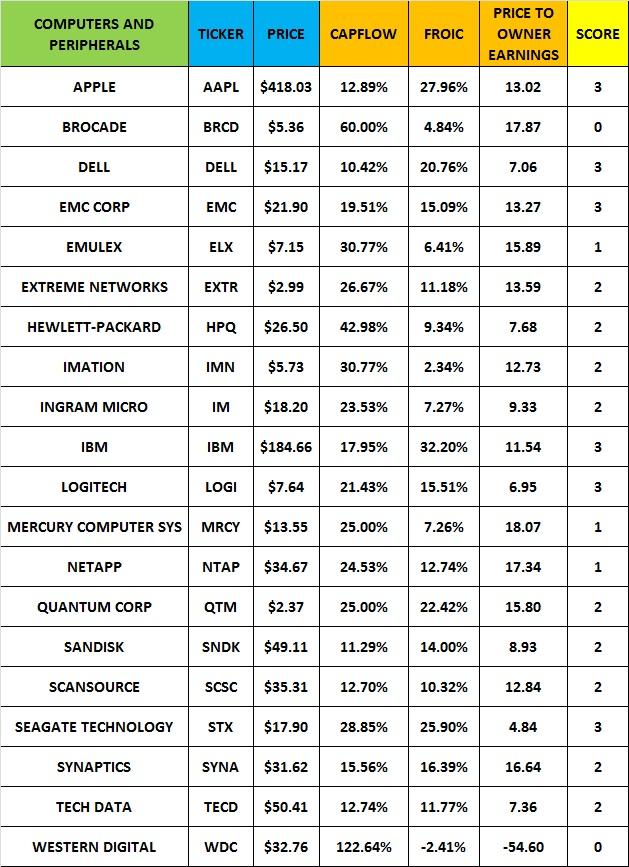

Before continuing with our analysis of Apple let us first look at their competitors and see how they are doing from an owner earnings perspective. The following is a table of the major companies that are in Apple?s Industry: (Click to enlarge)

As you can see from the table above, with my system you can zero in (within minutes) and know exactly which companies are the super stocks and which ones are the dogs with fleas. Western Digital (WDC) and Brocade (BRCD) are definitely dogs with fleas, as Western Digital comes in with two negative results and has a CapFlow of 122.64%. So one could say ?look out below!?

IBM (IBM) and Dell (DELL) are definitely super stocks as they are clearly putting up strong owner earnings numbers. Unlike Apple, Dell is concentrating on consumers who are looking for a low price point. In comparing the two, one finds that Dell's computers sell for about half of what Apple's do, but even so, Apple is winning in the owner earnings game because it gives its consumers "white glove" customer service and quality. In this world you get what you pay for.

IBM's long-time CEO recently retired and I am not sure how good its new CEO will be. So I will give her some time to show me what she can do before joining Mr. Buffett in buying it.

If you are looking for value plays, then Dell, Logitech (LOGI) and Seagate Technology (STX) have insanely low price to owner earning numbers. Had you done this analysis on Seagate back in September you would have had an amazing buying opportunity as the stock was only selling in the low teens. Here is a chart of Seagate that will clearly show you what can happen to you as an investor when you get the owner earnings numbers right: (Click to enlarge)

Finally one stock being pumped up by analysts is Hewlett Packard (HPQ) as Meg Whitman is now the CEO. But we need to give Meg some time to get things organized as the stock is still a value trap, in my opinion. I can say this because its FROIC is still too low for a tech stock and though its CapFlow is under 50%, it is not much below that. If Whitman can shed some assets that are underperforming and bring HP's FROIC up to 20%+, you may have a great turnaround story here.

Recently Apple's stock has been in a trading range even though its Owner Earnings numbers have been fantastic. I don't know if this is a result of its CEO Steve Jobs' passing, but I believe that I may have the answer as to why this may be happening. It can be attributed to the company having way too much cash on its balance sheet. This excess cash reduces the company's Main Street performance numbers because it effects its FROIC. Remember that FROIC measures owner earnings return on total capital. Total capital is basically long term debt + shareholder?s equity. Cash which returns 1% at best makes up the lion's share of Apple's total capital. In my opinion, Apple needs to either start making acquisitions of companies that have a FROIC of 20%+ or it needs to start paying a dividend. Until the company does that, I have decided to sit on the sidelines. As you can see, FROIC is actually expected to drop from 30.64% in 2011 to 27.96% for 2012, even though Apple's owner earnings are expected to grow at 27.02%.

You can?t really be expected to move much in the stock market if the return on half of your capital is growing rapidly and the other half is dead- growing at just 1%. It is an anchor on the stock, which can be remedied very quickly by paying a one-time $20 a share dividend to shareholders. Warren Buffett has this similar problem as Berkshire Hathaway (BRK.A) generates way too much cash. He solves this problem by being proactive about it and invests the cash in companies like IBM (IBM), Intel (INTC) or MasterCard (MA) which are all monster FROIC producers in their own right. If Apple's management decides not to pay out a dividend or buy out other companies, they should at least start buying stock in other companies which have tremendous FROIC. Until they do something about all that cash, the stock should remain in a trading range as much of its total capital is only earning 1% at best.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Disclaimer: Always remember that these are the results of our research based on the methodology that I have outlined above and in other articles previously published. This research is provided as an educational tool and should not be considered investment advice, but just the results of our research. There are many ways to analyze a stock and you should never blindly follow anyone?s work without doing your own due diligence or by seeking the help of an investment advisor, if you so need one.

x factor winner footlocker julia gillard julia gillard pecan pie the hobbit trailer prometheus trailer

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.